Thank you for joining us today for an overview of the SHOP Marketplace, and the application and enrollment process for SHOP coverage that starts in 2015. This presentation addresses the SHOP Marketplace run by the federal government known as the Federally-facilitated SHOP Marketplace and also as the FF-SHOP. States running their own SHOP Marketplace may operate differently. If youre unsure whether your state uses the Federally-facilitated SHOP.

Thank you for joining us today for an overview of the SHOP Marketplace, and the application and enrollment process for SHOP coverage that starts in 2015. This presentation addresses the SHOP Marketplace run by the federal government known as the Federally-facilitated SHOP Marketplace and also as the FF-SHOP. States running their own SHOP Marketplace may operate differently. If youre unsure whether your state uses the Federally-facilitated SHOP.Marketplace or runs its own SHOP Marketplace, please visit Healthcare.Gov for more information. This presentation is not intended for the press. If you are a member of the press or other media outlets, please contact the CMS press office for further information at press@cms.Hhs.Gov. This presentation is also available on Marketplace.Cms.Gov.

Finally, the information presented here is not intended as legal or tax advice. For such advice, we encourage you to contact a legal or tax professional. Thank you, and now, we'll begin. This presentation explains the features of the Federally-facilitated Small Business Health Options Program (FF-SHOP) and how these are changing for plan years starting in 2015.

During the presentation, we will cover the following topics: What the FF-SHOP is, Who can purchase FF-SHOP coverage and when Employee participation requirements for small group plans ACA standards and protections for SHOP Qualified Health Plans. How employers can browse their coverage options before buying Coverage options for the Self-Employed The Small Business Health Care Tax Credit The Employee Choice option The Small Business Health Options Program (SHOP), is part of the new Health Insurance Marketplace sometimes called an Exchange and is available in every state. It was created to make it easier for small employers to find and purchase health insurance for their employees. Some states are running their own SHOP Marketplaces, while others are participating in the Federally-facilitated SHOP Marketplace.

This presentation is focused on the Federally-facilitated SHOP Marketplace, also known as the FF-SHOP Marketplace. The SHOP is open to employers with 1-50 employees including non-profit and religious organizations. The FF-SHOP Marketplace offers a choice of health and dental plans, and tools to help customers make informed purchasing decisions. Employers and their employees can submit initial group enrollments for SHOP.

Coverage at any time throughout the year. After the initial group enrollment is submitted and coverage goes into effect, SHOP enrollments are limited to an annual enrollment period for employees, special enrollment periods, and enrollment periods for newly eligible employees. In addition, if employers offer their employees coverage through the SHOP, and meet other eligibility requirements, small employers may be able to claim a Small Business Health Care Tax Credit worth up to 50% percent of their premium contributions. Together, new insurance reforms and the SHOP will help curb premium growth, and spur competition based on price and quality.

The SHOP Marketplace now lets small businesses find and enroll in 2015 coverage online through HealthCare.Gov. And, in 14 of the 33 states using the FF-SHOP, small employers now have the option to offer their employees a choice of health plans, much like large employers do. Small employers with fewer than 50 full-time-equivalent employees aren't required to offer their employees health insurance, and theres no penalty if they choose not to. The FF-SHOP is open to small employers with 1 to 50 full-time equivalent employees (FTEs) Full-time equivalent employees generally include those who work at least 30 hours per week.

Part-time workers whose combined hours total at least 30 hours per week, are also included when determining FF-SHOP eligibility. Employers must have at least one employee on payroll, who is not a business partner or spouse, to be eligible for FF-SHOP coverage. To participate in the FF-SHOP employers must offer coverage to all employees who work an average of 30 or more hours per week. HealthCare.Gov now offers an online tool--the SHOP FTE.

Calculator--that can help employers count how many full-time equivalent employees they have, to help determine if they might be eligible for the Federally-facilitated SHOP. The FTE Calculator is based on the counting method used by the FF-SHOP which, until 2016, may differ from the method used by states running their own SHOP. Employers in a state with a state-based SHOP should contact the SHOP in their state to learn more. Small employers can offer employees health coverage through a FF-SHOP.

Now, or at any time during the year. In the FF-SHOP, if an employers initial group enrollment is completed between the 1st and 15th day of the month, coverage could begin as soon as the first day of the next month. For example, if initial group enrollment is completed on March 10, group coverage could begin as soon as April 1. For initial group enrollments completed after the 15th of the month, coverage could begin as soon as the first day of the second following month.

So, for enrollment completed on March 18, group coverage could begin as soon as May 1. Before employees can complete enrollment in an FF-SHOP plan, the employer will generally need to meet the FF-SHOPs minimum participation rate for their state. States and issuers may also set different requirements for group plans offered outside the SHOP. Marketplace.

In many states that are using the Federally-facilitated SHOP, at least 70% of the business or groups employees who are offered coverage must accept the offer before any employees can enroll. In a few states, the FF-SHOP has set a different minimum participation rate, so employers should check on HealthCare.Gov to find out if their state is one of these exceptions. An employers participation rate is determined by taking the number of employees who are enrolling in coverage offered through the SHOP, and dividing it by the total number of employees offered coverage. Not every employee is counted for purposes of determining the participation rate, such as employees with group coverage through another job, another persons employer health plan or through government-sponsored coverage such as Medicare, Medicaid, VA, Indian Health Service, or TRICARE.

An employees dependents also aren't counted in determining the participation rate. However, employees who are getting coverage through an individual health insurance plan are counted for the purposes of this calculation. Employers dont need to calculate their employee participation rate themselves, because the SHOP. Enrollment application will do this, and will determine whether the employer has met the minimum requirement, based on information provided by employees when they accept or waive the employers coverage offer.

There is an exception to these minimum participation requirements. From November 15 - December 15 each year, employers can buy small group coverage inside or outside the SHOP Marketplace without having to meet any applicable minimum participation requirement. Employers that offer employees SHOP coverage can be sure theyve selected a plan that conforms to the new standard. All health plans sold through the SHOP.

Marketplace are known as Qualified Health Plans and include a package of essential health benefits, like coverage for doctor visits, preventive care, hospitalization, and prescription drugs. Employers and employees buying group coverage will also have the benefit of an array of other consumer and insurance protections offered by the health care law. In the small group market, insurance companies generally must spend at least 80% of premium dollars on health care and quality improvement activities, and no more than 20% for other purposes, such as administrative, overhead, and marketing costs. Health insurance companies must also publicly disclose, justify and let the state or federal government review any rate hike of 10% or more, before raising premiums.

Health insurance companies cant sell plans that charge employers more because of a workers medical history, health condition or disability. Nor can they sell plans that charge more for women based on gender, and there are new limits on charging higher premiums for older employees based on age. Also, insurance companies now generally have to spread risk across a states small group market, rather than on a group-by-group basis. This should help make premiums more stable from year to year, over time.

Before employers begin their SHOP application, they can get a look at price estimates for all the 2015 Qualified Health Plans and Qualified Dental Plans that the Federally Facilitated SHOP. Offers in their area by using an online premium estimation tool. Users answer a few quick questions, such as whether they're looking for health benefits or dental benefits and select the state where their primary business address is located. The price estimates are based on the age-ranges of employees and where the business is located.

Estimates reflect prices for people who don't use tobacco. Insurers are allowed to charge higher premiums for tobacco users. Agents, brokers or Navigators can help employers use the tool and make plan comparisons. Once they're ready to apply for coverage, employers can get a final quote on HealthCare.Gov as part of the online enrollment process.

Neither the price estimates on HealthCare.Gov, nor the final quote will reflect any savings an employer might be eligible to receive through the Small Business Health Care Tax Credit after filing tax returns. Sole proprietors, or shareholders of more than 2% of an S corporation that has no common law employees, cant buy insurance through the SHOP. But small employersand spousesmay qualify to buy insurance through the Health Insurance Marketplace, which sells health insurance for individuals and families. Depending on the level of household income, as individuals, sole proprietors may qualify for tax credits through the Health Insurance Marketplace.

While small employers can complete an initial group enrollment at any time during the year, individuals using the Health Insurance Marketplace generally must enroll during the Open Enrollment Period. For 2015 coverage, Open Enrollment for individuals and families began on November 15, 2014 and continues until February 15, 2015. Outside of Open Enrollment, however, sole proprietors, the self-employed and their families may be eligible for a Special Enrollment Period in the Health Insurance Marketplace if there is a change in life situation, known as a qualifying life event, and in certain other, limited circumstances. Examples of qualifying life events include: moving to a new state, certain changes in income, and changes in family status or size like, if getting married, getting divorced or having a baby.

Visit HealthCare.Gov for more information on premium assistance, enrollment, and qualifying life events. The Small Business Health Care tax credit was created to help small employers of low-to-moderate-wage workers defray the costs of providing coverage. One important reason for employers to consider offering employees SHOP. Coverage is that, starting 2014, the credit is generally only available to those who have employees enrolled in SHOP coverage.

Employers may be eligible for the credit if they have fewer than 25 full-time-equivalent employees and those employees have average wages of less than $50,000 a year. The average salary limit is adjusted for inflation beginning in 2014. For practical purposes, that means that an employer whose employees wages average less than $51,000 may qualify for the credit in tax year 2015. The limit on employer size applies to full-time-equivalent employees.

That means that employers who have more than 25 lower-to-moderate wage part-time employees may still be eligible for the credit. For example, two half-time employees might equal one full-time-equivalent employee. Full-time equivalent employees are calculated differently for purposes of the tax credit than for determining whether an employer can use the SHOP Marketplace. The tax credit bases full-time equivalent employees off a 40 hour work week.

To be eligible for the credit, employers must also pay at least 50% of employees self-only health insurance premiums. The value of the tax credit increased significantly starting with tax year 2014, and is now worth up to 50% of the employers premium contribution (up to 35% for tax-exempt employers). For tax years 2010 through 2013, the credit was worth up to 35% of the employers contribution (25% for tax exempt employers.) Employers who offered employees health insurance during any of the years from 2010 to 2013, may still be able to claim the credit for those years, and should consult a tax advisor for more information. Starting with tax year 2014, the enhanced tax credit is available for two consecutive yearseven for employers that have already claimed the credit one or more times before 2014.

Since the Small Business Health Care Tax Credit became available in 2010, small employers have received more than $1.5 Billion in tax credits for contributions to employee premium costs. To help employers learn if they might be eligible for the tax credit, and how much that credit might be worth, HealthCare.Gov offers a tool, called the SHOP Tax Credit Estimator, available at the web address listed here. Small employers can now access the SHOP online at HealthCare.Gov to: - Browse, select and offer employees health and dental coverage that begins in 2015 - Have employees enroll in SHOP. Coverage online - Find and authorize a SHOP-registered broker to help with online enrollment Paper applications for SHOP coverage are no longer distributed or accepted.

SHOP-registered agents and brokers can access new online features and manage accounts when authorized by clients. Employers in 14 Federally-facilitated SHOP states can offer employees a choice of plans within a single plan category. The SHOP Call Center is now available to assist employees, as well as employers, agents and brokers. The SHOP Marketplace offers employers a choice of plan categories, insurance companies, and Qualified Health Plans.

Qualified Health Plans are grouped into 4 categories, each named for a precious metal: Bronze, Silver, Gold, and Platinum. Categories generally reflect how plans share the costs of care with the average enrollee. Plans share costs with enrollees through deductibles, copayments and coinsurance and out-of-pocket limits For example, the average employee in a plan at the Bronze plan category is expected to pay approximately 40% of covered medical expenses, and the plan is expected to pay approximately 60%. Please note, these percentages are for the average individual and may vary somewhat from individual to individual.

Generally speaking, Qualified Health Plans that pay a larger share of an employees medical expenses, also have higher premiums. As mentioned, all Qualified Health Plans in the SHOP must offer benefits from each of 10 essential health benefit categories defined in the law, such as coverage for doctor visits, preventive care, hospitalization and prescriptions. Still, Qualified Health Plans, even within a single plan category can differ in other wayssuch as in the networks of providers or the prescription drug formularies offered Grouping plans into metal categories allows consumers to compare plans with a similar level of cost sharing. This, along with consideration of premiums, provider networks, and other factors, can help the consumer make an informed decision.

Any employer who offered an FF-SHOP health plan to employees in 2014 and wants to renew that SHOP coverage, needs to do so online. Renewals cant be done for SHOP coverage by working directly with an insurance company. SHOP-registered agent or brokers also have to handle renewals and changes to SHOP coverage, online. Before beginning the renewal process, employers should consider the timing of their renewal offers, and keep in mind that they: - Must give employees at least one week to decide whether to accept the offer, and - Must submit enrollments by the 15th day of the month for coverage to start the first day of the next month When renewing SHOP participation online, employers will be asked the same questions asked on the 2014 application.

They should answer the questions based on information that applies for 2015with one important exception: - If an employer had 50 or fewer FTEs when enrolling in 2014 but now has more than 50 FTEs, that employer should attest to the statement that says the business has 50 or fewer FTEs, based on last years attestation. The SHOP is required to let an employer continue to participate in SHOP for 2015 if all of the following apply. The employer: - Received a determination of eligibility from the SHOP in 2014 - Had 50 or fewer FTE at the time SHOP. Participation began in 2014 - Added employees after beginning SHOP.

Participation and now has more than 50 FTEs - Meets all other requirements for participating in the SHOP If all of these factors apply, an employer can attest to having 50 or fewer employees based on the prior years attestation, and can continue to participate in the SHOP in 2015 The ultimate goal of SHOP is to give small employers more options for their employeesincluding the option to offer employees a choice among health plans at in one plan category. In 2014, small employers in states with a Federally-facilitated SHOP generally had a choice of health plans and dental plans in different plan categories, from various health insurance companies. Employers could select to offer employees only one SHOP Qualified Health Plan and, if applicable, a single SHOP Qualified Dental Plan. Some states running their own SHOP Marketplace gave employers the option to offer employees a choice of plans.

Now, employers in 14 states using the Federally-facilitated SHOP can offer employee choice. This means that an employer selects a plan category, and then the employee can enroll in any plan available within that category. Many states running their own SHOP Marketplace offer an employee choice options, which may differ from the employee choice option offered by the FF-SHOP Marketplace. In 2016, all states are expected to offer small employers a choice between offering employees a single SHOP plan, or letting employees select among multiple SHOP plans.

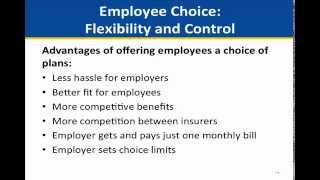

Offering employees a choice of plans can provide advantages for both employers and employees. Employee choice can mean less hassle for employers because they dont have to spend as much time trying to find one plan to fit all. It means that employees can select the plan that works best for their individual needs. Offering employees a choice of health plans--as many large employers docan help a small business help attract and retain valued employees.

And when employees can choose their own plan, insurers have to compete for their business which can lead to lower costs and better service. With the SHOP Marketplace more choice comes with less paperwork: no matter how many different insurance companies or plans employees select, the employer gets and pays just one monthly bill. The SHOP takes care of disbursing payments. Employees get choice, but the employer sets basic limits, by deciding which category of plans to offer, and how much to contribute to premium costs.

In 2015, in 14 of the 33 states using the Federally-facilitated SHOP, small employers can offer their employees a single qualified health plan and, if they choose, a single dental plan. Alternatively, they can let their employees choose a plan within the plan category the employer selects. In those states using the FF-SHOP and offering employee choice, employers can offer employees a choice among all qualified health plans in a single plan category that the employer selects. If applicable, the employer can also offer employees a choice among all dental plans within a single plan category that the employer selects.

In any state using the FF-SHOP, an employer can still choose to offer employees a single qualified plan and (if applicable) a single dental plan, if the employer prefers. The FF-SHOP offers many ways to get help: The toll-free SHOP. Call Center offers assistance to employers, agents and brokers, and now also to employees enrolling in employer-offered SHOP coverage. Also, for coverage beginning in 2015, employers who create an online account in the SHOP Marketplace on HealthCare.Gov can find a SHOP-registered local agent or broker online, and can authorize that agent to help with enrollment and to manage the employers SHOP account online.

Employers can also use the Find Local Help feature on HealthCare.Gov to locate a SHOP-registered agent or broker, or other assisters in their area, without creating an online SHOP account. Employers just enter their city and state, or their zip code, and select the Small Business Health Options box. Employers who want to work with an agent or broker they found through Find Local Help, should ask the agent or broker if he or she has registered with the SHOP Marketplace and has completed a SHOP. Marketplace profile.

Only agents and brokers who have taken these steps can complete an application for an employer. The SHOP Marketplace offers a simpler way to find, and compare health insurance and dental insurance options for small employers and employees. New online features put the whole enrollment process online at HealthCare.Gov for coverage beginning in 2015. Beginning with tax year 2014, small employers may qualify for a tax credit worth as much as 50% of their contribution to employee premiums when they buy coverage through the SHOP Marketplace and meet other eligibility requirements.

HealthCare.Gov offers straightforward information, useful links to information about how the ACA affects small business and helpful tools, like the SHOP FTE Calculator, SHOP Tax Credit Estimator, and the Premium Estimate Tool Employers get a choice of health plans from multiple insurance companies, and in different plan categories. Small employers in the 14 Employee Choice states now have the option to choose a plan category and let employees select any plan in that category. Help is available and easy to find, through the HealthCare.Gov Find local help tool, the SHOP Call Center, and through the searchable online list of FF-SHOP-registered agent or brokers thats available through the SHOP. Application.

For information about the FF-SHOP Marketplace and online tools, visit Healthcare.Gov/small-businesses. The IRS has in-depth information about the Small Business Health Care Tax Credit on its website. CMS.Gov/CCIIO is the website for the federal Center on Consumer Information and Insurance Oversight, and has detailed regulatory information and guidance for the SHOP Marketplace, as well as a resource page for Agents and Brokers, and information about other assisters. Finally, to get news about the SHOP Marketplace, in 2015, online tools and tips for small business owners, new health plans and prices, and more, we encourage you to sign up for SHOP Email Updates at the web address listed in the box on your screen.

Thank you again for joining us today..

No comments:

Post a Comment